Taxpayers will have until Tuesday, April 18, 2017 to file their 2016 returns and pay any taxes due. That’s because of the combined impact of the weekend and a holiday in the District of Columbia.

Taxpayers will have until Tuesday, April 18, 2017 to file their 2016 returns and pay any taxes due. That’s because of the combined impact of the weekend and a holiday in the District of Columbia.

WASHINGTON — The Internal Revenue Service announced today that unclaimed federal income tax refunds totaling more than $1 billion may be waiting for an estimated 1 million taxpayers who did not file a 2013 federal income tax return.

For many taxpayers, the dread of gathering information, preparing a tax return, and filing it is tedious and time consuming. However, just as the sun shines brightest after a rain, cheers and smiles replace the angst of prep when the tax refund check makes its way to the bank account.

“I’m going to … take a trip, buy a TV, go shopping…” After all, a common thought when receiving the refund is “it’s my money AND it is a refund! I should live a little.”

If you discover an error after filing your return, you may need to amend your return. The IRS may correct mathematical or clerical errors on a return and may accept returns without certain required forms or schedules.

In these instances, there’s no need to amend your return. However, do file an amended return if there’s a change in your filing status, income, deductions, or credits. Use Form 1040X (PDF), Amended U.S. Individual Income Tax Return, to correct a previously filed Form 1040 (PDF), Form 1040A (PDF), Form 1040EZ (PDF), Form 1040NR (PDF), Form 1040NR-EZ (PDF), or to change amounts previously adjusted by the IRS.

You can also use Form 1040X to make a claim for a carryback due to a loss or unused credit; however, you may also be able to use Form 1045 (PDF), Application for Tentative Refund, instead of Form 1040X. Also, if the Form 8938 (PDF), Statement of Specified Foreign Financial Assets, applies to you, file it with an annual return or an amended return. See the Form 8938 Instructions for more information.

Learn more about income tax planning from the Zinner & Co. tax team

Con artists often approach victims in their native language, threaten them with deportation, police arrest and license revocation, among other things.

“These scammers continue to adapt and evolve, and the IRS continues to receive reports of these schemes using multiple languages trying to find victims across the country,” IRS Commissioner John Koskinen said.

read more…

Many clients ask if it is more advantageous to pay quarterly tax estimates or utilize their tax withholding. I wish there were a simple, cookie-cutter answer. However, as no two taxpayers are alike, the same goes for the manner in which one can pay one’s taxes.

Both methods of paying income tax have their pros and cons. The best selection depends on your personal preference and, more so, financial situation. A majority of self-employed individuals must utilize quarterly payments. However, if you have an income source such as retirement distributions, social security or employee wages, you have the option of withholding tax from those income streams in lieu of paying quarterly. read more…

A dangerous email scam currently is circulating nationwide and targeting employers, including tax exempt entities, universities and schools, government and private-sector businesses. The scammer poses as an internal executive requesting employee Forms W-2 and Social Security Number information from company payroll or human resources departments. They may even send an initial “Hi, are you in today” message before the request.

For some, a simple flip through the day’s mail can soon turn into a panic-producing event. Bad news, bill collectors, or worse, a tax notice from the IRS, state department of taxation, or the local tax agency.

read more…

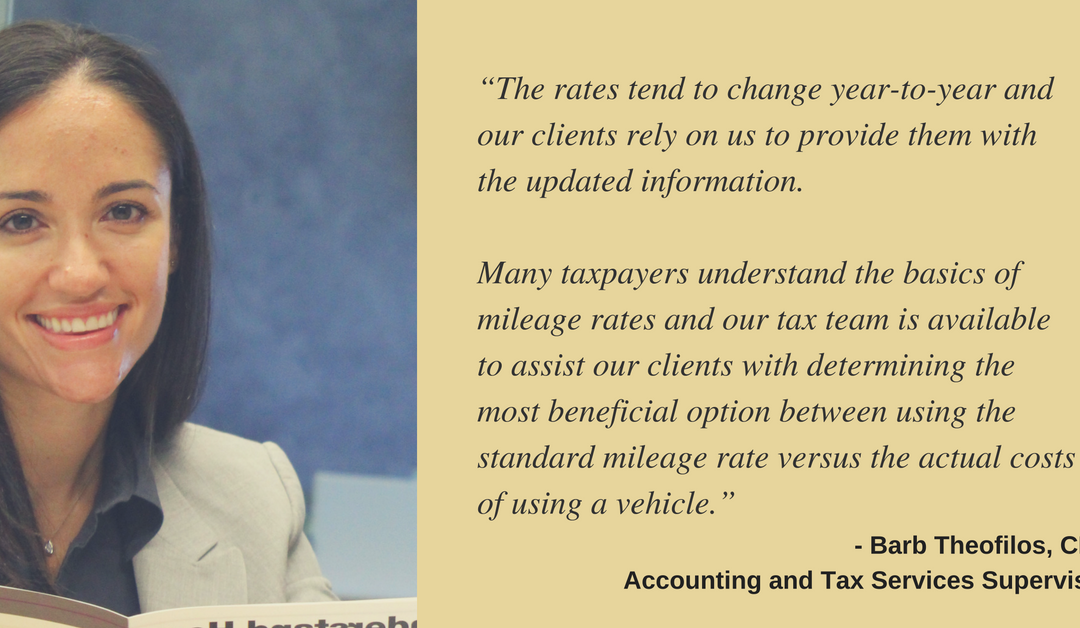

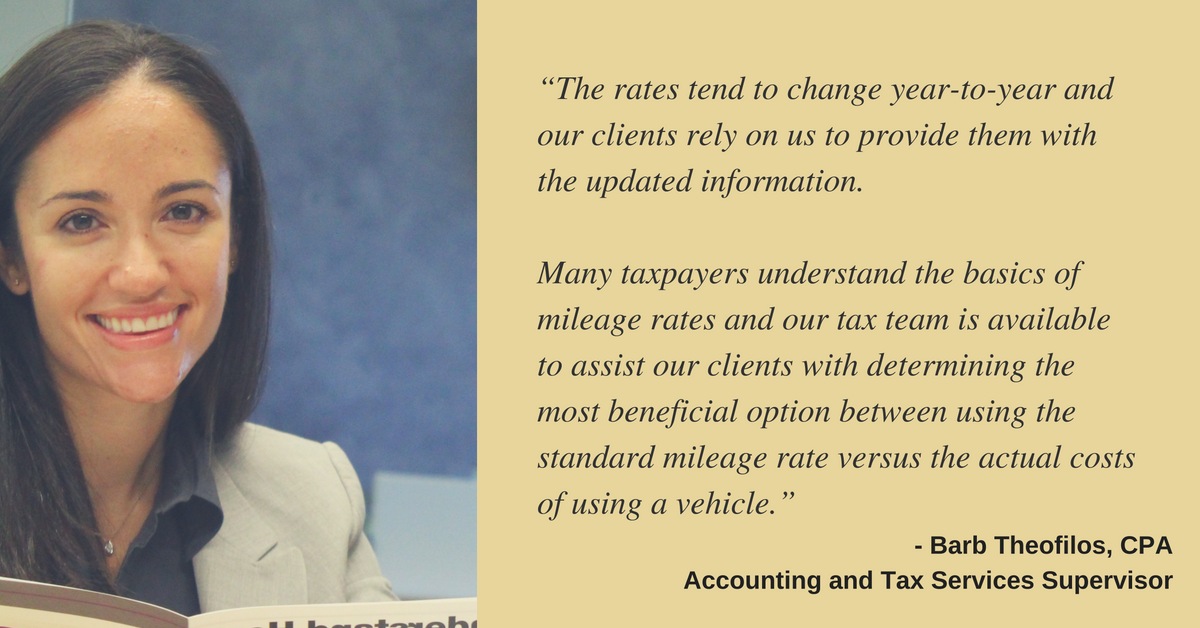

The Internal Revenue Service has issued the 2017 optional standard mileage rates to calculate the deductible costs of operating an automobile for business, charitable, medical or moving purposes.

Does your nonprofit organization and its donors understand the IRS requirements surrounding charitable donations?

A nonprofit organization that does not understand the details of the IRS requirements, is not able to effectively communicate to donors, or provide donors with accurate and appropriate documentation, can risk alienating donors. In addition, an organization could potentially miss an opportunity to increase donor giving levels and on the flip side, could be exposed to monetary penalties.

To promote charitable giving, the IRS allows for tax deductions for contributions of cash or other monetary and non-monetary gifts as long as certain recordkeeping requirements are met.

Folks can generally only deduct charitable donations to qualified organizations, such as places of worship and nonprofit organizations/hospitals (i.e., Colleges, United Way, Girl Scouts). If you’re not sure that the organization you plan on making a donation to qualifies, ask them, or you can check the following website: (www.irs.gov/Charities-&-Non-Profits/Exempt-Organizations-Select-Check). Keep in mind that you cannot obtain a charitable donation deduction for contributions to individuals, or for the value of your time or services provided to an organization.

Once you’ve determined that the organization is qualified, you need to make sure that you’re going to obtain a tax benefit by making the donation. If you don’t itemize your deductions (file a Schedule A), you will not have the ability to deduct the amount donated. Also, you cannot (generally) deduct charitable contributions that exceed 50% of your Adjusted Gross Income (“A.G.I.”). Finally, if you’re A.G.I. is above a certain threshold (in 2016, $311,300 if you file jointly, $259,400 if you file as a single taxpayer), your total charitable contributions, as well as your other itemized deductions (i.e., real estate taxes, mortgage interest) may be limited.

Let’s take a look:

Monetary gifts (cash, checks, payroll deductions, stock gifts, etc.)

To validate a deduction taken for a charitable contribution of any amount, the taxpayer (the one claiming the deduction on their tax return) must have:

Often, such contributions are made through payroll deductions to or facilitated by organizations such as the United Way. In these instances, the taxpayer must maintain a pay stub or Form W-2. The taxpayer may also furnish another employer-generated document that details the amount(s) withheld for payment to the charitable organization, along with a pledge card filled in by or at the direction of the donee charitable organization. These basic documentation rules apply to all gifts unless a gift individually exceeds $250.

Read more from Chris Valponi

Additional requirements for gifts of $250 or more state that the taxpayer must obtain:

Keep in mind that for payroll deductions, the IRS states that the contribution amount withheld from each paycheck to a taxpayer is treated as a separate contribution for purposes of applying the $250 threshold. To illustrate, 15 payroll deductions of $20 each, totaling $300 over the course of the year would not be considered to meet the additional requirements threshold of $250.

read more…

More and more third parties are looking at not-for-profit organizations’ IRS Form 990, so don’t just report; learn how you can use your 990 to tell your organization’s story. The 990 is an annual informational tax return that is required to be filed by not-for-profit...

Part 5 of a 5 Part Series Can board members be held personally liable for actions of the organization? Yes! Agreeing to sit on a board for a nonprofit is a great way to donate your time and expertise. However, it comes with a great deal of responsibility. Board...

Estimates show that over 5% of all revenue is lost to fraud and theft each year. The numbers are staggering - odds are if you have not experienced it, you will. One of the best ways to prevent fraud and theft is to implement a system of internal controls (though no...

One of the fastest and most effective ways to gain momentum and market share is through the acquisition of a competitor. Acquiring a competitor has two distinct advantages – it allows you to eliminate competition; and it allows you to gain new products,...

Did you receive an Ohio Individual Income Tax Failure to File notice (ITDQ0009) from the Ohio Department of Taxation (ODT) advising you that they did not receive an Ohio Individual Income tax return? Starting December 8, 2016, ODT began sending notices to...

Send us your questions and we’ll share our insights with you on our blog!